You have insurance for your car, your health, your home, and your life. So why not insure your career? Physical therapy liability insurance can protect you in the event of a malpractice lawsuit, helping you dodge hefty indemnity claims, legal fees, and license defense costs.

As physical therapists, we don’t like to entertain the idea of getting sued by our patients or their families—isn’t compassionate care and diligent documentation enough? Not necessarily, as we’ll see in this post. Carrying a personal policy for professional liability insurance may feel like overkill, but when compared to the cost of the average indemnity claim, you may conclude it’s more than worth it.

What is Physical Therapy Liability?

As a physical therapist, you’re liable for the quality of care you provide: from proper management of the patient’s treatment plan to oversight of their condition and the safe administration of treatment modalities. No PT is perfect, and even an occasional mistake can precipitate harsh consequences.

A patient or their family can sue for a number of reasons. The patient could fall on your watch. They could sustain a bad burn from a malfunctioning TENS unit at the clinic. If you misread the physician’s orders and led an exercise they weren’t ready for—say, resisted active range of motion in a post-surgical patient—they could sue. The worst cases involve not just pain and inconvenience, but hospitalizations, additional or worsened injuries, infection and even death.

Who Can Get Sued?

Whether you’re a student, a Physical Therapist Assistant or a full-time PT, you could be liable for injuries incurred under your care. Self-employed PTs who own their practice risk having their business sued. As long as you’re interacting directly with patients, you are liable for their wellbeing.

Even the most experienced therapists among us are at risk of a lawsuit. In fact, 34% of claims in this FSBPT study were made against therapists with 21 years or more experience—the highest percentage of therapists under a malpractice lawsuit.

Below is a table of claims made against PTs, PTAs, and PT students, those individually insured and those insured through their PT practice. Notably, these only include claims with paid indemnity of $10,000 or more.

Common Circumstances for Getting Sued

According to the HPSO 2020 Claim Report, over 60% of malpractice claims involve fractures, worsened injuries, burns, or falls. Fractures are the most common reason for a lawsuit, featuring in over 28% of the closed claims paid in 2020.

These injuries happen most often, plaintiffs claim, due to one of the following allegations:

- Improperly managed care over the course of treatment

- Failure to supervise or monitor the patient

- Improper performance of therapeutic exercise

- Improper performance of manual therapy

- Malfunctioning equipment

If the PT is found liable, each of these allegations can have steep consequences. Check out the table below for the average total incurred for these top-dollar allegations in 2020:

Going Uninsured Is Getting Expensive

If you’ve followed physical therapy liability over the last decade, you’ll notice that the costs involved have all increased. Paid indemnities have gone up, and so have the average legal costs for defending oneself against allegations, both in court and before state boards.

For example, the average total cost for claims incurred by PT professionals in 2020 was $134,761, an increase of more than 12% from the 2016 average of $119,893. The average cost to defend an allegation was $14,575 in 2020, up from 2019’s $13,635. From 2016 to 2020, the average cost for defending a license increased 18% from $4,828 to $6,020.

| Average cost | 2016 | 2020 |

| Total claim | $119,893 | $134,761 |

| Allegation defense | $13,635 | $14,575 |

| License | $4,828 | $6,020 |

Physical Therapy Liability Insurance: Low Premiums with Ample Coverage

What’s stayed low and affordable through it all are the premiums for physical therapy liability insurance. One provider, My PT Insurance, charges employed PTs just $150 per year for liability insurance. Student PTs can pay as little as $25, while self-employed PTs can get annual coverage for just $300.

Despite the low premium, My PT Insurance offers ample coverage to protect you in some of the most severe cases of malpractice. Their professional liability policy can cover up to $1 million in fees and damages per occurrence, and as much as $3 million in one year. Considering that most claims are settled for far less than a million, you can rest assured the policy from My PT Insurance is more than enough to cover your backside.

Still unconvinced it’s worthwhile? Consider how much a physician or surgeon has to pay to protect their career. Malpractice insurance for a physician can cost several thousand dollars annually, even $50k, $100k, or an outrageous $200k in some parts of the country for certain branches of medicine.

For us PTs, it’s much simpler. Less than $300 a year can safeguard a self-employed PT from $3 million worth of allegations against professional liability, general liability, or product liability.

Types of Insurance Policies

When shopping for physical therapy professional liability insurance, you’ll come across two types of policies: occurrence and claims-made. Let’s take a closer look at what either option offers.

Occurrence coverage protects you from claims that are made for something that happened while your policy was active. The occurrence of the alleged malpractice determines whether your policy applies.

Claims-made coverage, by contrast, protects you as long as the claim is made while your policy is active.

For example, let’s say your patient suffers a fall in October 2023 but doesn’t submit a claim until January 2024. If you have occurrence coverage for 2023 only, then you’ll still be protected from the January claim, even though your policy has lapsed. With claims-made coverage, however, your policy would only apply if the patient made the claim on December 31, 2023, or earlier.

The best strategy is not to let your coverage lapse, but occurrence policies can protect you retroactively even when it does. The professional liability coverage from My PT Insurance is occurrence-based, protecting your liability when your policy was active, not when the claim was made.

What Does PT Liability Insurance Cover?

The particulars of your liability insurance can vary based on your insurance provider. For comprehensive coverage, look for a policy that offers the following:

- Coverage for License Defense or a HIPAA Infraction Defense

- Reimbursement for First Aid or Medical Payment expenses

- Reimbursement for Lost Wages from court proceedings

- Coverage for Personal Injury costs or Property Damage

- Coverage for Sexual Misconduct allegations

- Defense Attorney Provision and Deposition Fee coverage

- The option for Portability in case you change employers or clinics

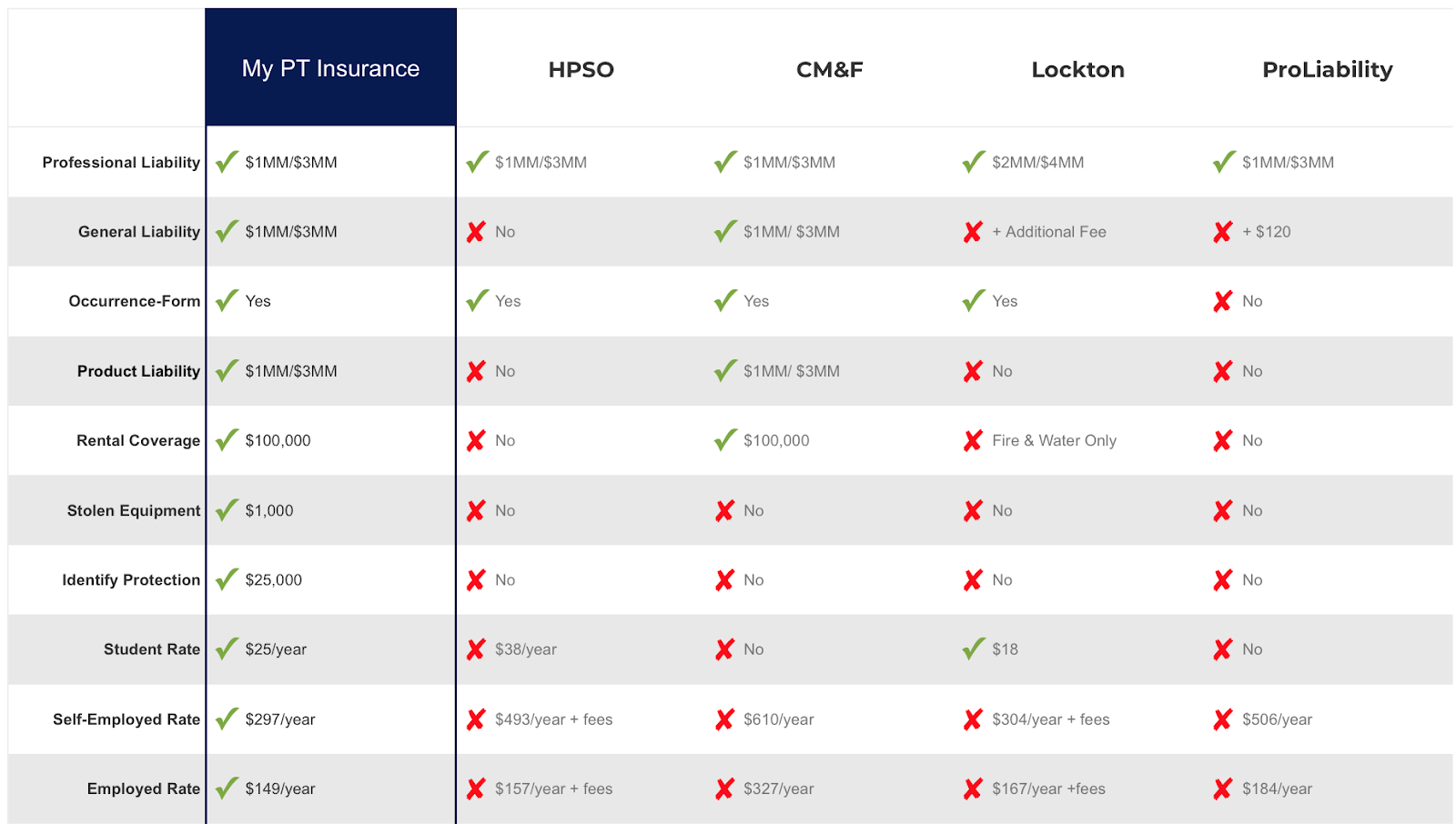

If you choose My PT Insurance, you’ll automatically get much of this coverage, and more. See how they compare with the competition:

What If I’m Covered by My Clinic?

Many clinics have general liability insurance, and some even hold a separate policy to protect their therapists and employees. However, your clinic’s coverage might not be enough to protect you from hefty legal fees.

First of all, under a clinic’s insurance you can’t control the type of policy—whether occurrence or claims-made, for example. Your clinic’s policy may only cover basic liability without reimbursing for lost wages, attorney fees, or deposition fees.

Secondly, without personal liability insurance you leave yourself unprotected if you perform any PT work outside the clinic, such as during home visits or while freelancing.

As for the myth that carrying personal liability insurance makes you a target for litigation, that’s been mostly debunked. Your liability policy is not a matter of public record, so there’s little credence to the idea that an insured PT is more likely to get sued than an uninsured one.

This article isn’t meant to serve as legal advice, however. Research your clinic’s policy, request a quote for a policy of your own, and consult a professional to help you make the decision that will best protect you and your career.

Summary

If you don’t want to pay a six-figure indemnity claim and potentially lose your license, consider getting professional liability insurance from My PT Insurance. At $150 per year, you’ll hardly notice it—until that unlucky event when you do.